Benchmark for broiler chicken 2024 – How has market-driven animal welfare developed since 2018?

The work to promote market-driven animal welfare in Denmark gained momentum in 2017 with the introduction of a three-level voluntary state animal welfare label for pork. In 2018, a similar animal welfare label was introduced for chicken meat. The benchmark project has so far followed this development from 2018 to 2024.

At the beginning of the period, the retail chain COOP had its own four-level scheme, but this was discontinued at the end of 2022 and the products were placed under the state brand.

Before 2018, there were not many alternatives to standard broiler production. There was organic broiler production, where the chickens had access to outdoor areas, and where the broiler chicken lines used grew much slower than the usual fast-growing broilers. In addition, slow-growing free-range chickens were imported from abroad, especially from France, where the alternative "label rouge" chicken production had been available for many years. These brands were and still are supported by Animal Protection Denmark.

The 2018 state animal welfare label for chicken focused on a new type of slower-growing chicken. The production of chickens with a welfare heart was therefore based on chickens that grew a little more slowly (typically around 50 g per day) than the usual chickens (which grow about 65 g per day), but not as slowly as the organic chickens (which grow about 30 g per day).

The development from 2018 onwards was influenced by campaigns from animal welfare organizations against the so-called "turbo chickens" (fast growing chickens). Several retail chains committed to selling chicken meat only from slower-growing chickens, at least in their range of fresh chicken meat, while others chose to have an assortment allowing customers to choose between fast-growing standard chickens and chickens with an animal welfare label.

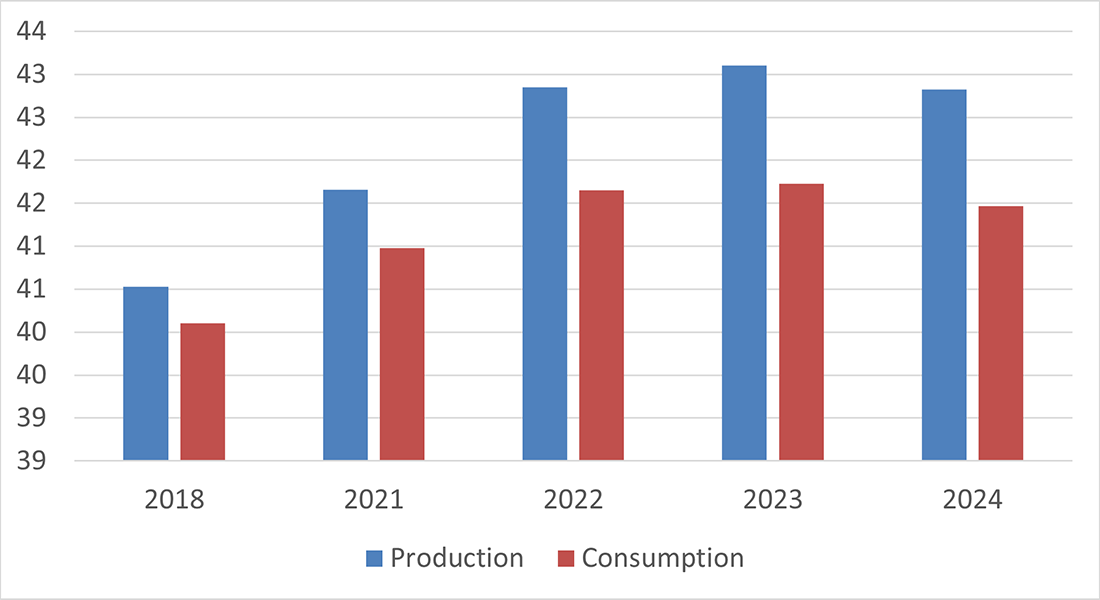

As shown in Table 2, at the beginning of the period, there was strong development in both production and consumption of chickens with a welfare label, with an almost fivefold increase in production and a more than sixfold increase in consumption from 2018 to 2021. After. 2021 this growth slowed and 2023-24 saw an actual decline. Danish broiler companies, which invested in a conversion to welfare chicken, have reported challenges in to selling the welfare chickens at a higher price. This is probably related to inflation and high food prices following the Covid crisis and the war in Ukraine. Although Danish finances in general improved in the latter part of the period, a crisis awareness seems to have taken hold.

Note that the term welfare chicken is used here for all types of broiler chickens that have a welfare higher than required by Danish legislation.

Table 2: The total Danish production of broiler chicken 2018-2024 together with the shares of welfare broilers in national production and consumption.

| Production (million broilers) |

Share of welfare broilers (% of production) |

Share of welfare broilers (% of consumption) |

|

|---|---|---|---|

| 2018 | 103.7 | 5% | 4% |

| 2021 | 102.2 | 22% | 23% |

| 2022 | 101.1 | 33% | 33% |

| 2023 | 102.7 | 37% | 39% |

| 2024 | 105.3 | 31% | 33% |

Note: The term welfare broiler is used here for all types of broilers from production systems offering welfare exceeding the requirements of Danish legislation. Percentages are based on volumes. The production volume is the number of broilers slaughtered in Denmark. In addition, around 14 million broilers are slaughtered abroad each year.

Stagnation in sales of welfare chickens is also reflected when the welfare of the Danish chickens is measured using the Benchmark method. Here, the relative contributions from different production systems are aggregated to a single Benchmark value for each individual year for production and consumption respectively (see Figure 5). Note that the scale in the figure is very detailed, which highlights the relatively small differences in the Benchmark values.

The benchmark method is described in more detail above, and specific information on the method's use in broiler chicken follows below.

More on the development of the consumption of welfare chickens in Denmark

In 2024, a total of 105.3 million chickens were slaughtered in Denmark (an increase of 2.5% compared to 2023). After a large decrease in organic chicken production of 63% from 2.3 million chickens in 2022 to 850,000 organic chickens in 2023, approximately 1.5 million organic chickens were slaughtered in Denmark in 2024. (Note that according to Statistics Denmark's organic statistics, 1 million organic chickens were slaughtered in 2024, but the industry estimates that this is too low, so the number is here estimated to be 1.5 million organic chicken.)

From 2021 to 2023, there was an increase in the production of welfare chicken (which is defined as all production with welfare levels higher than conventional production) from 22% in 2021 to 37% in 2023. This was followed by a drop again in 2024 to 31% of production. The vast majority of welfare chicken are produced with improved indoor conditions. For example, 22% of the production in 2024 consisted of 1 heart chicken production and only 9.1% of production achieved 2 hearts in the welfare labelling scheme. A further 4.4% of the chickens were given 3 hearts, divided into 3.4% free-range and 1% organic. In addition, in 2023, a small proportion of chicken were produced under the European Chicken Commitment (ECC) brand for the German market. The proportion of ECC chicken was 0.5% in 2023 and 0.3% in 2024.

A number of chickens are also sent for slaughter, mainly in Germany, but also in the Netherlands (according to the industry). For example, we have data that 13 million chickens were slaughtered outside Denmark in 2023 and 14.5 million chickens in 2024 (of which approximately 200,000 were organic chicken and the rest were conventional). If the foreign-slaughtered chickens are included in the production share, then the share of welfare chickens produced will fall from 31% to 27% of production.

The picture for consumption looks more or less the same as for production. Chicken with one or more welfare labels is almost exclusively produced for the domestic market. In addition, a significant proportion of free-range chicken consumption consists of imported chicken, mainly from France (about 2/3 of free-range chicken consumption is imported). In 2023, approximately 20% of organic consumption was also imported, however, we do not have information on whether this is also the case in 2024. A very large proportion of chicken meat is sold with private labels (in the order of 60% in 2024), of which a third of the fresh meat comes from heart 1 chickens.

There are significant exports and imports of chicken meat – in the order of 40% exported and 40% imported. To calculate Benchmark values, it is assumed that no welfare chicken are exported, except for the mentioned ECC chicken. Thus, it is estimated that almost all exports are standard chicken, while a relatively large part of the consumption of free-range and partly organic chicken is imported.

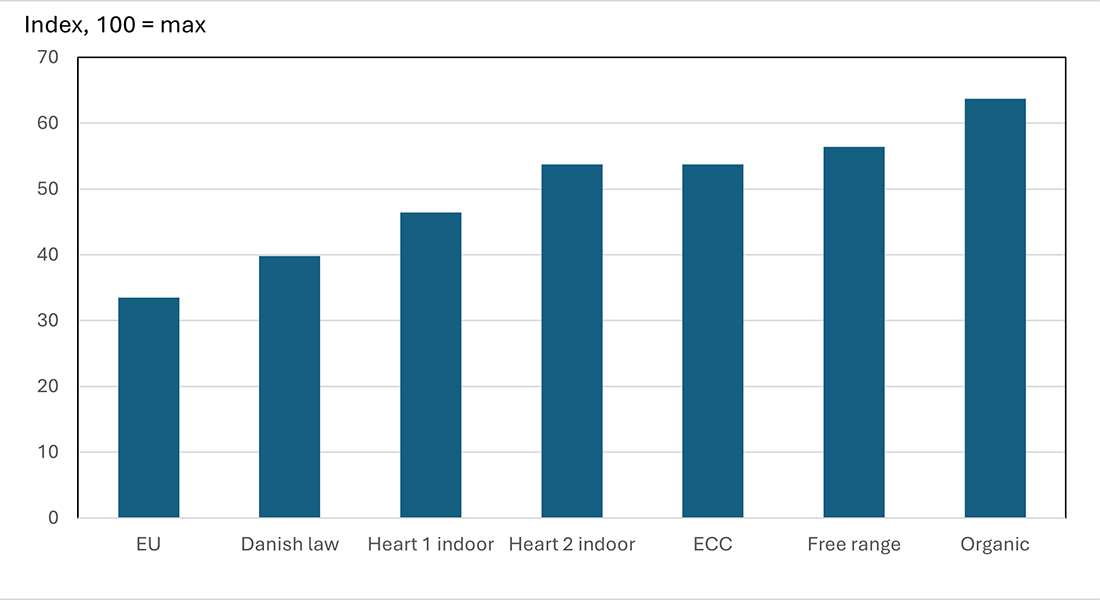

How much difference is there between animal welfare in different forms of production?

For chicken, the production types are divided into the legislative minimum, the 3 hearts from the Better Animal Welfare labelling scheme (where we divide heart 3 into free-range chickens and organic respectively) and the production of chicken that meet the requirements of the European Chicken Commitment (ECC). The difference between welfare measured by the Benchmark method is shown in Figure 6.

As shown in Figure 6, welfare, measured by the Benchmark method, increases steadily across the brands, with greater welfare the more hearts. All three levels of the voluntary state animal welfare label, Better Animal Welfare, require the use of slower-growing chicken breeds. This means that they must grow more slowly than standard chickens, which grow on average about 65 g per day, which is believed to increase the risk of a number of welfare problems. Chicken with one heart live indoors all their lives, but are slower growing and have a little more space per chicken; with two hearts, the chickens also have access to roughage or other material to serve as enrichment. Chickens produced with three hearts, are typically much slower growing and have access to outdoor areas. Three-hearts production includes both free-range chicken and organic chicken, but we divide then here for two reasons: First, organic farming places more demands on promoting animal welfare in production than the free range system does. Secondly, there may be both free-range and organic production that does not use the Better Animal Welfare labelling scheme.

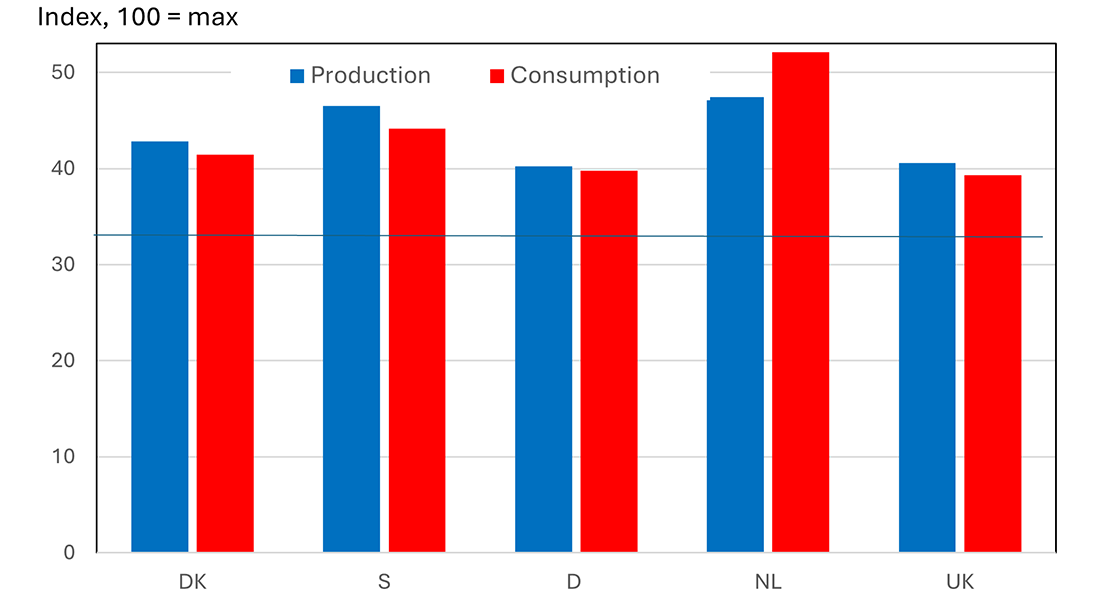

Comparing Benchmark values across countries

The Benchmark method makes it possible to compare animal welfare across countries in a systematic way. The figure below compares the benchmark values for broiler production and national consumption in five Western European countries (Denmark, the Netherlands, the United Kingdom, Sweden and Germany).

There are clearly differences between countries in terms of how good chicken welfare is. The higher the Benchmark value, the better the welfare opportunities. Denmark is in the middle of the field in terms of both national production and national consumption of chicken meat – the estimated Benchmark value for Denmark is slightly higher than that for Germany and the UK, but lower than that for Sweden and the Netherlands.

Detailed explanation of results

For each country, there is a benchmark value for both national production and national consumption. When the two values differ, it is because chicken meat is also exported and imported. For the Netherlands, the benchmark value is significantly higher for consumption than production. For the other countries, the two values are very close, but with a slightly higher value for production than consumption.

This is because even though consumers in these countries consume the majority of national production, made for brands that focus on animal welfare, large amounts of chicken meat are imported that have been produced with minimum animal welfare requirements. The retail trade and the catering sector, together with some consumers in these countries have the effect of pulling the overall welfare of national chicken consumption down to a level below the standard of national production. The contrast is greatest in the country with the highest national production standards, namely Sweden.

The exception to this picture is to be found in the Netherlands, as already mentioned. Here we estimated a higher benchmark value for national consumption than for national production. This is mainly due to two factors: first, in the Netherlands, supermarkets have succeeded, with the support/pressure of animal welfare organisations, in agreeing that all fresh chicken meat sold is from slower growing chicken breeds with improved animal welfare. Secondly, the Netherlands has a large export-oriented production of standard chicken.

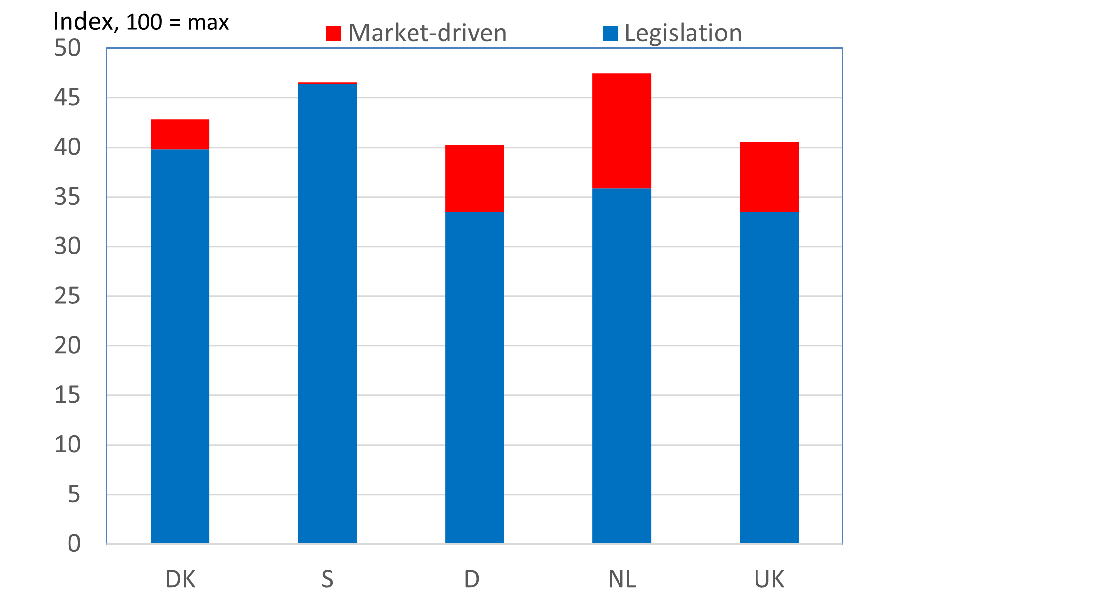

The horizontal line in the figure indicates minimum requirements for the welfare of chickens, as defined by the EU. This is expressed in a directive with minimum requirements for animal welfare, to which each country must adapt its national legislation. The fact that production in all countries has a higher benchmark value compared to the EU's minimum requirements has two different explanations:

In the case of Denmark and Sweden, the explanation is primarily that the two countries have legal requirements that go beyond the EU minimum. For example, both Denmark and Sweden have a requirement to assess foot pad dermatitis in broilers (and to pursue follow-up activities if the values are too high), while this is not an EU requirement. For the other three countries, however, the explanation is primarily market-driven initiatives. The legal requirements for keeping and caring for chickens kept for meat production are in line with, or only slightly above, the EU minimum requirements.

Both legislation and market-driven initiatives have had an impact on the estimated benchmark values. Differences in the relative importance of legislation and market-driven initiatives are very clear when comparing Sweden and the Netherlands. Sweden has the most far-reaching legislation to ensure the welfare of broiler chickens in national production. In the Netherlands, it is mainly market-driven initiatives that have taken the Benchmark value for national production above the EU requirements, and the Benchmark value of domestic consumption higher than it is in Sweden.

The market-driven initiatives include the fact that all fresh chicken meat sold in Dutch supermarkets comes from slower-growing chickens. The situation in Denmark is somewhat similar to Sweden, with relatively high regulatory standards, combined with nationally produced welfare chicken, counteracted by imports of cheap chicken meat produced according to lower animal welfare standards.

Through various initiatives it is possible to reach a relatively high welfare level in both production and national consumption. In terms of production, this is clearly illustrated by the following figure, which shows the relative importance of legislation and market-driven initiatives in relation to national production.

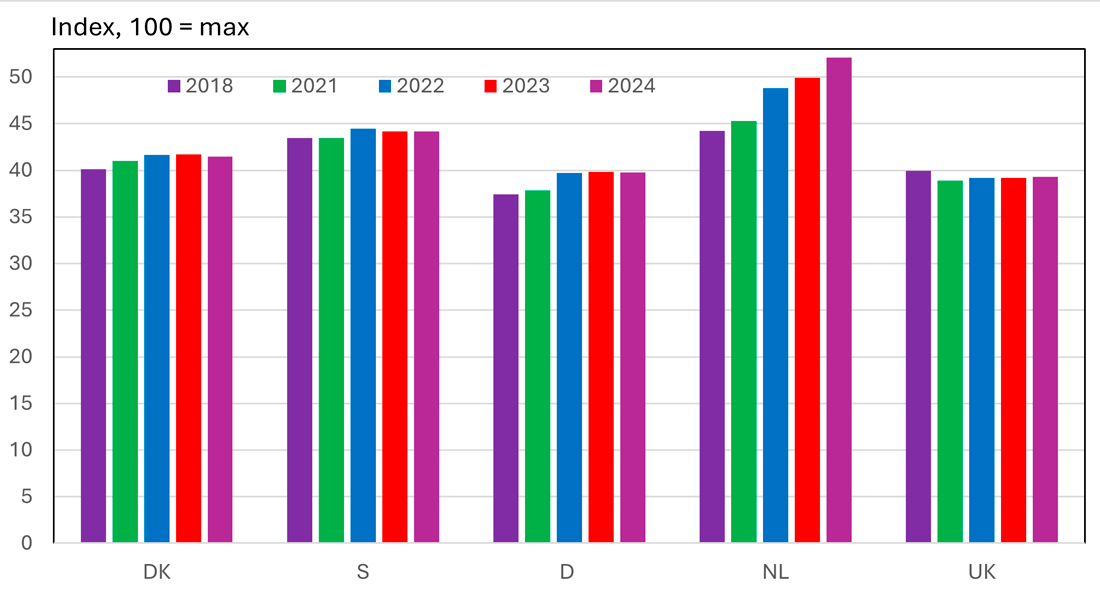

Developments in the five countries from 2018 to 2024

The following two figures show the development of benchmark values for national production and national consumption of chicken meat in the five countries.

The most significant finding is an increase in benchmark values in the Netherlands, driven by supermarkets supplying fresh chicken meat only from slower-growing chickens – meaning that consumers have no option to buy cheaper chicken products from standard chickens.

In three of the countries, Denmark, Sweden and Germany, there was a slight increase in the estimated consumption benchmark up to 2022. This was primarily provided by nationally produced slower-growing broilers. However, these markets have stagnated or declined in recent years due to higher food prices and uncertainty. For Denmark and Germany, there is a corresponding decline in the production benchmark at the end of the period, while the benchmark for Swedish production is stable.

At the same time, the development of imports of cheap chicken meat from countries with lower welfare standards has been counteracted. In the period 2018 to 2023, there was an almost fivefold increase in imports of poultry meat from Eastern Europe, especially Poland.

Limitations

As with all other methods for making wider comparisons of animal welfare, the Benchmark method has several general limitations. The most important of these are described under the Benchmark method.